JobKeeper Extension 1 Commences Soon

As the original JobKeeper comes to an end at the end of this week, we welcome JobKeeper Extension 1 on the 28 September, the first of two separate extension periods.

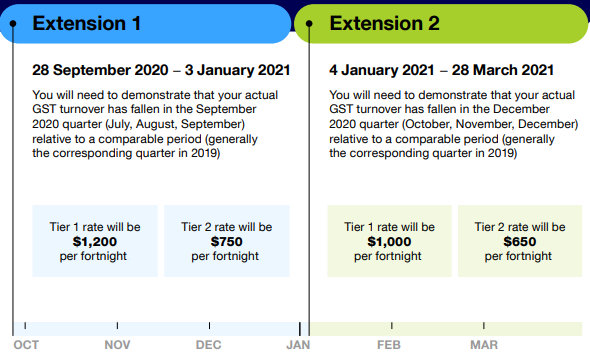

This extension period will run from 28 September 2020 to 3 January 2021.

Payment Rates

As mentioned in our previous communications, the rates of payment will change. Current fortnightly payments are $1,500 (before tax), but JobKeeper Extension 1 rates will depend on the number of hours an eligible employee works or business participant actively engages in the business.

Tier 1 rate of $1,200 per fortnight (before tax)

- Eligible Employees: Worked a minimum of 80 hours in the four weeks of pay periods before either 1 Mar 2020 or 1 July 2020.

- Eligible Business Participants: Actively engaged in the business for a minimum of 80 hours in February 2020 and provide a declaration to that effect.

Tier 2 rate of $750 per fortnight (before tax)

- This rate applies to any other eligible employees and eligible business participants.

Eligibility

To be eligible for this first extension program, you will need to show that your actual GST turnover has declined by the specific shortfall percentage (30%, 50% or 15%) in the September quarter (July, August, and September) to a comparable period (usually the corresponding quarter in 2019).

What do I need to do?

Commencing 28 September 2020, you need to:

- work out if the tier 1 or tier 2 rate applies to each of your eligible employees and/or eligible business participants and/or eligible religious practitioners

- notify us and your eligible employees and/or eligible business participants and/or eligible religious practitioners what payment rate applies to them

- during JobKeeper extension 1 – ensure your eligible employees are paid at least

- $1,200 per fortnight for tier 1 employees

- $750 per fortnight for tier 2 employees.

If you are registered for GST and have outstanding BAS statements, you should lodge your BAS for the September 2019 and December 2019 quarters as soon as possible (or for equivalent months, if you report monthly). Un-lodged BAS statements may hold up your application for JobKeeper Payments under the JobKeeper extension.

For many businesses registered for GST, this calculation will match the ‘total sales’ reported at G1 on your BAS minus GST payable (1A), where applicable.

If you are not registered for GST, you will work out your turnover using either the GST cash or non-cash basis of accounting.

You can provide additional turnover information to demonstrate that you satisfy the actual decline in turnover test for the September quarter from the start of October onwards. You must provide it before you complete your November monthly declaration.

Alternative tests for determining actual decline in turnover may be available in some circumstances. These will apply in a similar way to the alternative tests for the original decline in turnover test. However, they must be applied on the basis that the turnover test period is a quarter. ATO will publish more information on the alternative tests for the actual decline in turnover test once it becomes available.

If organisations do not meet the turnover test in the extension period this does not affect their eligibility prior to 28 September 2020.

Please contact us if you require assistance.

——–

Source: https://www.ato.gov.au/General/JobKeeper-Payment/JobKeeper-extension-announcement/

Date Posted: 23 September 2020